Operating a money transfer or remittance business without the required authorisation is a serious regulatory offence in Australia and most global jurisdictions. Regulators treat unlicensed money transfer activities as high-risk because they expose the financial system to fraud, money laundering, terrorism financing, and consumer harm.

Businesses that operate without a valid money transfer business licence face severe legal consequences, including heavy fines, criminal prosecution, forced shutdowns, and permanent reputational damage. Below is a clear breakdown of what operating without a licence means, the risks involved, and why compliance is critical.

What Does Operating Without a Money Transfer Licence Mean?

Operating without a licence means providing money remittance or transfer services without meeting mandatory regulatory requirements, including AUSTRAC registration, reporting obligations, and ongoing compliance. This includes:

- Running a domestic or international remittance service without approval

- Transferring funds through agents or third parties without authorisation

- Continuing operations after a licence has expired, been suspended, or revoked

- Failing to meet ongoing AML, KYC, or reporting obligations.

Even unintentional non-compliance can trigger enforcement action.

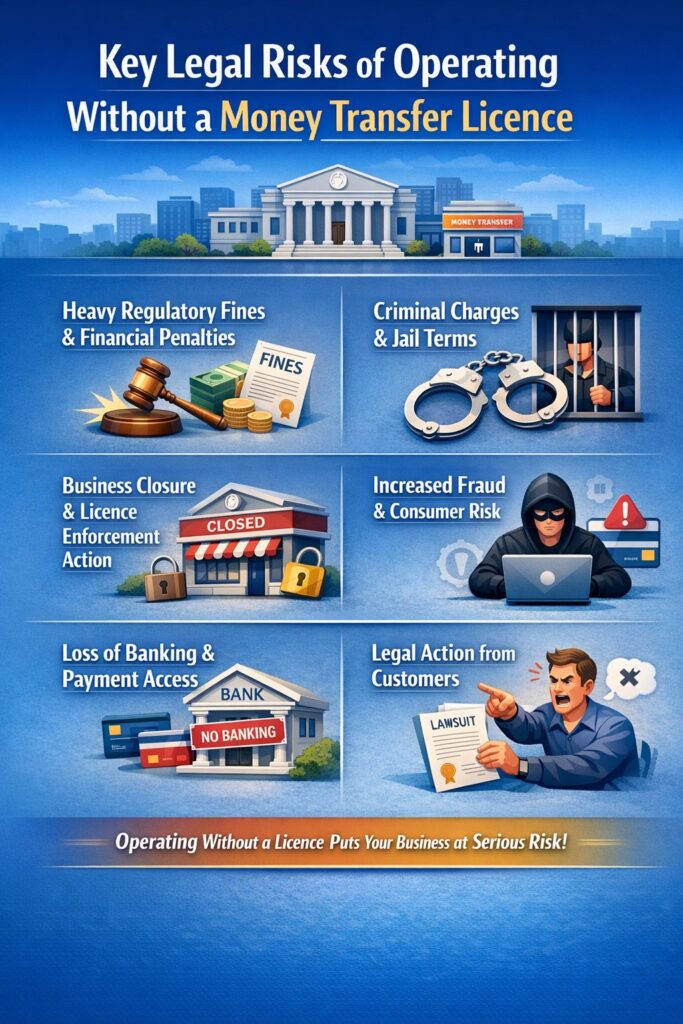

Key Legal Risks of Operating Without a Money Transfer Licence

Heavy Regulatory Fines and Financial Penalties

Regulators can impose substantial fines for each breach of licensing laws. In many cases, penalties increase per transaction or per day of non-compliance. Fines can quickly exceed the cost of obtaining a licence, making non-compliance financially devastating.

Criminal Charges and Jail Terms

Serious or repeated violations may result in criminal prosecution, including:

- Jail terms for directors or operators

- Criminal records

- Court-ordered business shutdowns

Unlicensed money transfer activity is often treated as a serious financial crime, not a minor administrative issue

Business Closure and Licence Enforcement Action

Regulators have broad enforcement powers, including:

- Immediate cease-and-desist orders

- Forced business closure

- Asset freezing or seizure

- Long-term regulatory monitoring

Once enforcement action is taken, obtaining a licence later becomes significantly more difficult.

Increased Fraud and Consumer Risk

Unlicensed money transfer businesses are frequently associated with:

- Higher fraud risk

- Loss or misuse of customer funds

- No consumer protection or compensation mechanisms

This exposes both customers and business owners to severe financial and legal losses.

Loss of Banking and Payment Access

Banks, payment processors, and financial institutions typically refuse to work with unlicensed operators. Common consequences include:

- Frozen bank accounts

- Terminated merchant services

- Inability to process transactions

Without banking access, a money transfer business cannot operate.

Legal Action from Customers

Customers harmed by unlicensed operations may pursue civil claims for:

- Financial losses

- Breach of trust

- Misrepresentation

These lawsuits add to regulatory penalties and long-term reputational damage.

Why Do Money Transfer Regulations Exist?

Money transfer regulations are designed to protect both consumers and the financial system by ensuring:

- Transparency in financial transactions

- Prevention of money laundering and terrorism financing

- Secure handling of customer funds

- Accountability of financial service providers

Failing to comply places your business in direct violation of financial law and triggers swift regulatory response

Common Non-Compliance Violations and Penalties

Violation Type | Possible Consequences |

Operating without a licence | Heavy fines, business closure |

Breach of licence conditions | Regulatory penalties, audits |

Repeated offences | Criminal charges, jail terms |

False or missing reports | Licence suspension or revocation |

Ignoring compliance checks | Increased enforcement action |

Can You Fix the Issue After Being Caught?

In limited cases, regulators may allow businesses to apply for a licence after enforcement action, but this comes with:

- Increased scrutiny and investigations

- Delayed approvals

- Reduced chances of success

- Higher compliance and legal costs

It is always safer, faster, and more cost-effective to secure the correct licence before starting operations.

How to Avoid These Risks

To operate legally and securely:

- Register with AUSTRAC before providing services

- Implement AML and KYC compliance frameworks

- Maintain transaction monitoring and reporting systems

- Conduct regular compliance audits

- Seek professional licensing and compliance support

A compliant business is trusted, scalable, and protected.

Facing challenges with money transfer services? Contact our experts

Operating a money transfer business without the required licence is a high-risk decision with serious legal, financial, and reputational consequences. The cost of non-compliance far outweighs the time and expense of proper licensing.

If you plan to operate a money transfer or remittance business, securing the correct licence, meeting compliance obligations, and maintaining regulatory standards is essential for long-term success. Contact us +61-423-989-900 to speak with compliance experts and start your money transfer business the right way.

Frequently Asked Questions About Operating without a money transfer licence

Is it illegal to operate a money transfer business without a licence?

Yes, operating without the required licence is illegal in most jurisdictions and can result in fines, criminal charges, or business closure.

What fines apply for unlicensed money transfer operations?

Penalties may include heavy regulatory fines, seizure of funds, licence enforcement action, and possible jail terms for serious offences.

What are the legal risks of running an unlicensed money transfer business?

Legal risks include fines, forced shutdowns, lawsuits from customers, loss of banking access, and long-term reputational damage.

Can regulators shut down my business for not having a licence?

Yes, regulators can issue cease-and-desist orders, freeze accounts, and permanently close unlicensed businesses.

Does operating without a licence increase fraud risk?

Yes, unlicensed businesses face higher fraud risk and are often targeted for financial crime investigations.

Is AUSTRAC enforcement severe in Australia?

Yes, AUSTRAC enforcement in Australia is strict, particularly for unlicensed operations and AML/CTF breaches. Regulators actively monitor compliance and have the authority to impose fines, issue enforcement notices, and pursue criminal action when necessary.

How long does a compliance investigation take?

A compliance investigation can take several months and may extend longer depending on the complexity of the case, transaction volume, and level of cooperation. Investigations often involve audits, document reviews, and ongoing reporting requirements.

Can non-Australian companies operate here?

Yes, non-Australian companies can operate money transfer services in Australia, but they must register with AUSTRAC, meet all AML and KYC obligations, and appoint local compliance contacts where required.

How quickly can you get licensed once non-compliance is discovered?

Licensing after non-compliance typically takes longer due to increased scrutiny. Approval timelines vary, but applications may face delays of several months as regulators conduct additional reviews and assessments.